|

RCBJ-Audible (Listen For Free)

|

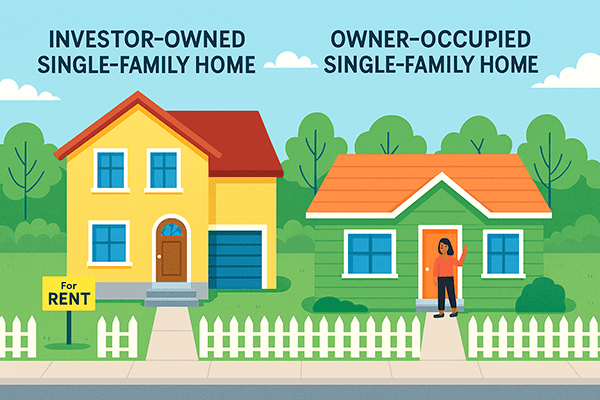

Local Tax Assessors Don’t Recognize Investor-Owned Single-Family Homes As Commercial Properties When Setting Tax Assessments

By Rick Tannenbaum

They are everywhere in Rockland County – single-family homes purchased by anonymous LLCs and rented out for profit. Some investors own dozens of homes, either in their own names or through single-purpose entities.

The increased involvement of corporations and private equity firms in the Hudson Valley real estate market is associated with heightened gentrification and displacement of existing residents in the region. Large and small corporate interests are driving prices up and out of reach for many tenants, making it exceedingly difficult for first-time homebuyers to enter the market.

Investors purchasing and renting out single-family homes are able to deduct all maintenance expenses on the home and grounds, interest on their mortgages, depreciation on the property, management expenses, legal, insurance and countless other categories of expenses that make the investments profitable, essentially sheltering the bulk of the rental income from state and federal income taxes. Municipalities incur costs to register and inspect investor-owned homes for habitability and code compliance.

Despite the incentives investors enjoy, these income-producing properties are assessed and taxed at the same rate as owner-occupied homes sitting next door and across the street because New York State assessment tax policies do not recognize the difference between investor-owned rental properties and owner-occupied single-family homes.

Orangetown Assessor Brian Kenney says, “Single family rentals are still considered typical residences or homestead properties, whether rented or not – and not commercial with higher tax rates. Non-Homestead, or commercial residences must have at least four units or more to be in that class.”

Local assessment practices are dictated by state law that establishes dozens of specific use codes for assessment purposes. The New York State Department of Taxation & Finance (NYSDTF) details nine particular “classification” codes: agricultural; residential; vacant land; commercial; recreation and entertainment; community services; industrial; public services; and wild, forested, conservation lands and public parks.

Within each category, are subcategories. For example, the residential category has subcategories for single, two-family, and three-family year-round residences, large estate properties, and seasonal use residences. There is no subcategory for single-family homes used as investment properties.

The commercial category has subcategories for apartments (usually four or more units), boarding houses, and “converted residences” (usually a single-family home that has been converted into a professional office or medical use). Single-family homes used as residential rentals are not classified as commercial uses.

“The state sets the property type classification codes. Assessors are required to follow them,” said Clarkstown Assessor John Noto.

And while the NYSDTF says municipalities “may use their own coding scheme, in addition to the codes” it provides, municipal assessors feel bound by the state categories and regularly bless single-family investment properties with the same assessments and lower taxes that owner-occupied homes in residential neighborhoods pay.

The acquisition of single-family homes by corporate interests picked up after the 2008 foreclosure crisis and has accelerated since the 2020s. Investors are disproportionately acquiring lower-priced properties with extensive deferred maintenance and marketing them as rental properties.

Local governments have established rental registries in their town and village codes to track the proliferation of conversions from owner-occupied homes to tenant-occupied homes and to insure that the rental market properties are code-compliant and safe. But code enforcement officers have trouble keeping up with complaints. Municipalities also require registration to insure that single-family homes are not divided up into apartment units, or utilized as boarding houses for day workers or transients.

LLC-acquired homes dot residential neighborhoods, but in actuality function as commercial investments. Despite the conversion to commercial properties, New York State’s assessment practices essentially preclude local assessors from imposing assessments reflective of the commercial investments made by LLC owners.

The Hudson Valley Pattern For Progress recently received a grant to undertake a study of the breadth and impact of corporate ownership of single-family homes in the Hudson Valley. That study should also look at the property tax impact of the existing assessment advantage investment properties enjoy.

Local municipalities have an inventory through rental registries of investor-owned properties. Given the growth in investor-owned residential homes in Rockland County and the Hudson Valley, and the ever-increasing tax burden necessary to maintain local governments, the NYSDTF and local assessors should consider establishing a new category to properly assess the value of investor-owned single-family residences and eliminate the tax advantage they enjoy via the omission in the assessment classifications.